Construction Loans

Build your dream home your way5.64%Variable Rate*

5.66%Comparison rate*

What’s the difference?

Construction Loan Vs Home Loan

Construction Loan

Perfect if you’re building your home, renovating heavily, or doing a knock-down rebuild. You pay interest only on the funds drawn at each stage — meaning lower costs during the build.

Home Loan

Ideal for purchasing an established property. Move-in ready or lightly cosmetic work only.

First time buyers are eligible for higher loan to value ratio with no additional costs*.

The ‘must knows”

Why choose a construction loan?

Interest only periods

during construction

during construction

Pay as you build

stage by stage

stage by stage

Perfect for new builds and or renovations

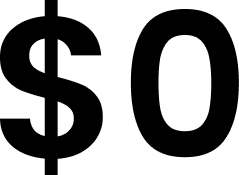

Pay $0 fees to us

for your application

for your application

Save more with

stamp duty exemption

stamp duty exemption

Refinance later to

maximize savings

maximize savings

Attention first timers!

Land & build packages

Your new land

ANy of these jobs most likely qualify for a professional home loan at 90% LVR with little to no LMI!

Build your home

This is the premium home loan tier for professionals. Borrow up to 95% LVR with zero LMI, saving thousands upfront.

How much can you borrow?

Use our borrowing power calculator to see how much money you can borrow for your construction loan

(HINT: enter the rate 6.99%, because we can achieve that!)

No pressure. No credit hit. Big potential reward.

Construction loan process

30 minute free

consult

consult

Tell us your situation and what you’re aiming to get out of your construction finance

1

compare & find

the best deal

the best deal

We’ll do the hard work and find you the best construction loan options, to make the best decision

2

Start progress

payments

payments

Once approved you’ll be able to take out your first drawdown and start building!

3

1

30 Minute Free

Consult

Consult

Tell us your situation and what you’re aiming to get out of your construction finance

2

Compare & Find

the Best Deal

the Best Deal

We’ll do the hard work and find you the best construction loan options, to make the best decision

3

Start Progress

Payments

Payments

Once approved you’ll be able to take out your first drawdown and start building!

What are you waiting for?

Get started with a free chat

No obligation, just guidance…

Get started with a free chat

No obligation, just guidance…

We compare all the banks for you

Don’t worry we’ve got your back every step of the way

Live human support

24/7

Contact us to discuss your questions with a real human

Up to and over

+100

Free accessible videos, articles, and tools designed to ease your journey

30 minute consultation

For Free!

Want direct help? No worries. Stop waiting and book your free consult immediately!

Still got questions?

Answer to your questions

How does a construction loan differ from a standard home loan?

Unlike a traditional home loan that provides a lump sum upfront, a construction loan releases funds in stages, known as “progressive drawdowns”. You only pay interest on the portion of the loan that has been drawn down to pay your builder for completed work. Once construction is finished, the loan typically reverts to a standard principal-and-interest mortgage.

What are the typical stages of a construction loan drawdown?

Most construction loans follow a 5-stage payment schedule: Slab (foundations), Frame (walls and roofing), Lock-up (windows and doors), Fit-out (plumbing and electrical), and Completion (final detailing). As each milestone is reached, your builder issues an invoice, which Loanity helps process so the lender can release the next payment directly to the builder.

Will I have to make full mortgage repayments while my house is being built?

No. During the construction phase—usually for up to 12 to 24 months—most lenders only require interest-only repayments on the funds that have already been released. This keeps your monthly costs lower while you may still be paying rent or living elsewhere during the build. Full principal and interest repayments generally only start once the final payment is made to the builder.

What documents do I need to provide for a construction loan?

Beyond your standard income proof, lenders require build-specific documents including a fixed-price building contract, council-approved plans, and a copy of your builder’s license and insurance. At Loanity, we coordinate with your builder to ensure all technical paperwork meets the lender’s specific requirements for a “tentative on-completion” valuation.

Can I get a construction loan if I am self-employed or a contractor?

Yes, self-employed borrowers can access construction finance through “Full Doc” or “Low Doc” options. While major banks often want two years of tax returns, Loanity has access to specialized lenders who may accept BAS statements or an accountant’s letter to verify your income. This is ideal for tradespeople and business owners whose income may be irregular due to project cycles.

Can I use a First Home Owner Grant (FHOG) toward my construction loan?

Yes, construction loans are a primary way for first home buyers to access government grants and stamp duty concessions. These incentives can often be applied at the land settlement stage or toward your initial deposit, significantly reducing your upfront cash requirement. We’ll assess your eligibility for all current state and federal schemes during your application.